Business Valuation Guide

Income-Based Business Valuation

A quick look at business valuation under the income approach shows that you have two key types of methods available:

- Earnings capitalization methods.

- Income stream discounting methods.

Given these two ways of doing the same thing you may wonder:

- Do these methods give the same business valuation results?

- Are there situations when capitalization or discounting methods are preferred?

As the math below demonstrates, there are specific situations when these two types of business valuation methods produce identical results. Strictly speaking, the following is true:

If the business earnings are unchanged or grow at a constant rate year to year, then the capitalization and discounting business valuation methods are equivalent.

This offers some useful insights:

- You can use the current year’s business earnings and earnings growth rate as your business valuation inputs.

- The capitalization rate is just the difference between the discount rate and the business earnings growth rate.

If business earnings vary significantly over time, your best bet is to rely on discounting when valuing a business. Since you can make accurate earnings projections only so far into the future, the typical procedure is this:

- Make your business earnings projections, e.g. 3–5 years into the future.

- Assume that at the end of this period business earnings will continue growing at a constant rate.

- Discount your projected business earnings.

- Capitalize the earnings beyond this point. This gives you the so-called residual or terminal business value.

The math

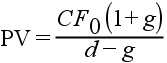

Take a look at the present value discount formula:

Where CF0 is the business cash flow as of the business valuation date, g is the constant annual growth rate in the cash flow, and d is the discount rate.

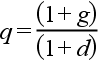

Now compare the above with the well-known result for the sum of the so-called geometric series:

Note that the present value is just the geometric series less the first term, which is equal to 1. Now make this substitution:

Which gives us the famous constant growth capitalization formula: